Machine learning in asset management helps investment firms turn raw financial data into structured signals for portfolio decisions. It supports return forecasting, risk monitoring, asset allocation, and trade execution using statistical and predictive models.

However, many investment teams face real pressure today. Markets react faster, and traditional factor models often struggle during regime shifts. At the same time, firms worry about overfitting, model drift, compliance scrutiny, and failed deployments.

In this blog, we will discuss what machine learning means in asset management, the models used, and data requirements. We will also discuss real applications, measurable benefits, and operational challenges.

What Machine Learning Means in Investment Asset Management

Machine learning in asset management refers to using data-driven models to support investment decisions. These models study past and live financial data to find patterns that humans often miss. Unlike fixed rule-based systems, they adjust as new data appears.

In investment teams, machine learning analyzes prices, returns, volatility, and macro signals. It can also read unstructured data, such as earnings call transcripts and financial news. This helps managers understand market behavior in a clearer and faster way.

Machine learning for asset management works as a support layer, not a replacement for professionals. Portfolio managers still decide what actions to take. The models simply provide structured insights that reduce guesswork.

At a basic level, machine learning helps firms process large datasets with consistency. It improves how teams evaluate risk, compare opportunities, and monitor portfolios in changing market conditions.

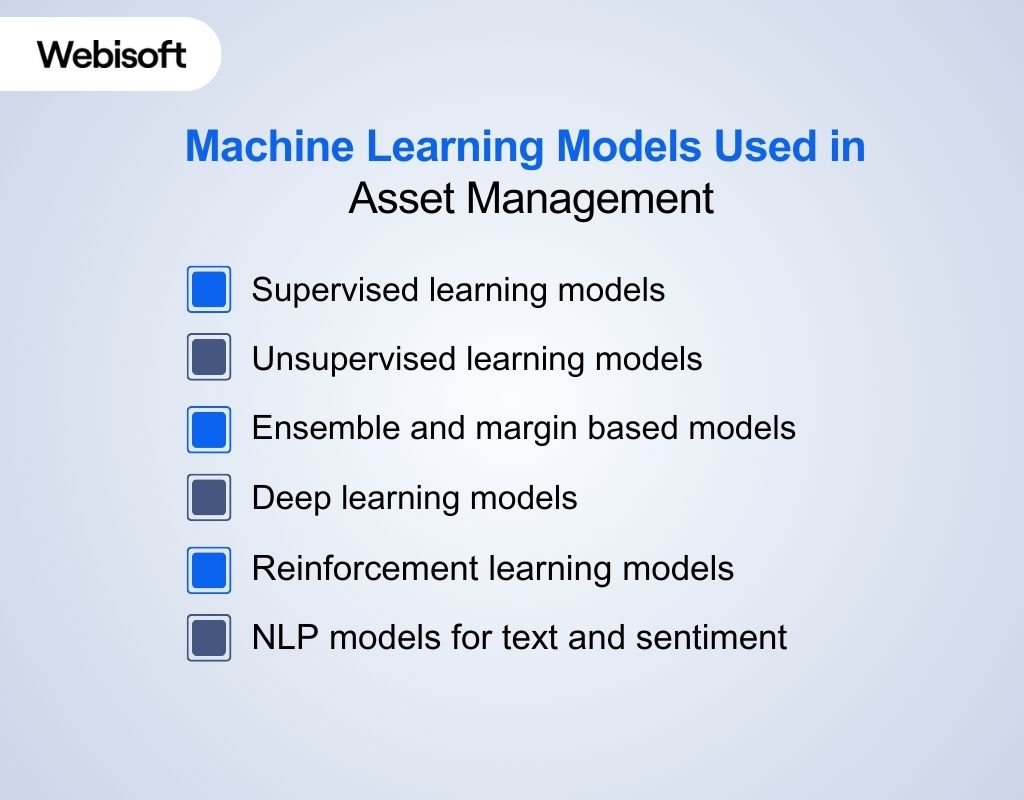

Machine Learning Models Used in Asset Management

This section explains the main model families teams use in investment workflows. Asset managers usually pick models based on the data they trust and the decision they need to make.

The CFA Institute Research Foundation even lays out dedicated chapters for unsupervised methods, support vector machines, ensemble learning, deep learning, reinforcement learning, and NLP in its 2025 monograph.

Supervised learning models

Supervised learning predicts a target you can label, like next month’s return bucket or a default risk score. In quantitative asset management machine learning, teams often start with linear models for simple signals and then move to trees or gradient boosted models when relationships bend.

These models work best when you can test them on clean history and keep the inputs stable over time. Teams use these models for ranking stocks, forecasting risk, and flagging drawdown risk early.

For example, a model can learn how valuation, momentum, and rate changes are linked to past outcomes, then score today’s universe with the same inputs. You still need strict validation, because financial data changes shape fast.

Unsupervised learning models

Unsupervised learning groups or maps data when you do not have a labeled target. Firms use it to cluster assets by behavior, spot hidden factors, and detect regime shifts without guessing labels first. Clustering also helps portfolio design when correlations jump around.

A simple example is grouping stocks by how they move in stress periods, then setting exposure limits per group. This approach often supports diversification decisions more directly than a single volatility number.

Ensemble and margin based models

Ensemble models combine many weak models to get a steadier signal. Teams use them because one model can overreact to noise, but a group can smooth errors. Support vector machines often help when you need a clean separation between classes, like risk on versus risk off days.

Ensemble trees often help when inputs interact, like rates, inflation, and sector flows moving together. These tools stay popular because they can perform well without the heavy computation of deep nets.

Deep learning models

Deep learning fits problems with lots of messy inputs and nonlinear relationships. Teams use it for time series patterns, cross asset signals, and some forms of volatility forecasting when simpler models miss shape. Deep models need strong controls, because they can learn noise that looks like signal.

You should expect heavier data cleaning, more compute, and more monitoring after launch. Regulators also warn about opaque decision-making and overreliance when firms use AI in investment services.

Reinforcement learning models

Reinforcement learning trains an agent to pick actions, then learn from rewards and penalties. In algorithmic trading machine learning, teams test RL for trade scheduling, market making, and position sizing, since the model can learn from simulated market impact.

According to a paper, they highlight portfolio management and execution as core RL targets in finance. RL can look strong in a lab but fail in live markets if the simulator misses real costs.

Teams need stress tests for slippage, fees, and changing liquidity before they trust outputs. This is why most firms treat RL as research first, then roll out narrow use cases.

NLP models for text and sentiment

NLP models turn text into signals you can test, like sentiment, topic shifts, or risk language. This matters because earnings calls, filings, and headlines move prices long before numbers hit spreadsheets.

The CFA monograph includes a dedicated NLP chapter, which reflects how common text features have become in investment research.

NLP often powers alternative data machine learning finance pipelines, especially when teams track news, transcripts, and event risk. A practical example is scoring an earnings call for uncertainty language and then checking how that score linked to future volatility in history. You still need governance, because data quality problems and bias can distort decisions.

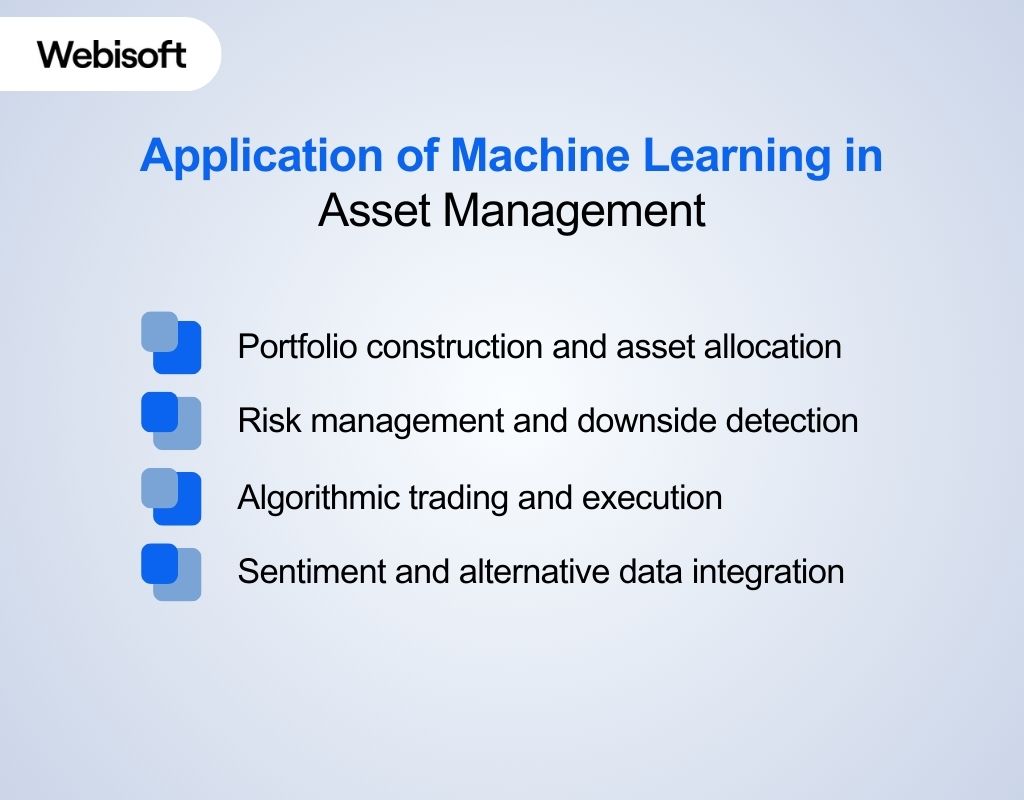

Application of Machine Learning in Asset Management

Machine learning in asset management has clear, measurable uses in forecasting, optimization, risk control, and execution. These applications go beyond theory and are tested on real financial data, not only backtested signals.

Portfolio construction and asset allocation

Machine learning helps investment teams select and weight assets based on complex patterns in returns and risk. For example, studies combining clustering with prediction models such as LSTM, CNN, Random Forest, and XGBoost show improved return forecasts and better portfolio construction than traditional forecasts alone.

Research also shows ML-driven parameters enhance dynamic allocation by improving both return and risk estimates compared to conventional optimization alone. The article shows how ML improves parameter estimation and optimization phases in asset allocation.

Risk management and downside detection

Asset managers use machine learning to monitor and limit downside risk by detecting abnormal volatility and stress signals across markets. Research shows that LSTM models combining forecasts with risk metrics like VaR and CVaR show superior performance over traditional econometric models in risk-aware forecasting.

ML risk models help teams quantify and mitigate exposures early, making risk management more reactive to market shifts.

Algorithmic trading and execution

Machine learning models, including reinforcement learning and deep architectures, guide trade execution by learning from historical market microstructure. The research illustrates how combined numeric and textual data improves portfolio decisions.

These models often outperform static strategies in simulated environments, but firms still layer controls and oversight for live deployment.

Sentiment and alternative data integration

Models that fuse textual sentiment with numeric indicators provide additional context for short-term trading and volatility signals. Research on ML designs integrates structured and unstructured data to improve decisions under real market stress.

This evidence confirms that ML is not only applied to price data but also to richer information sources.

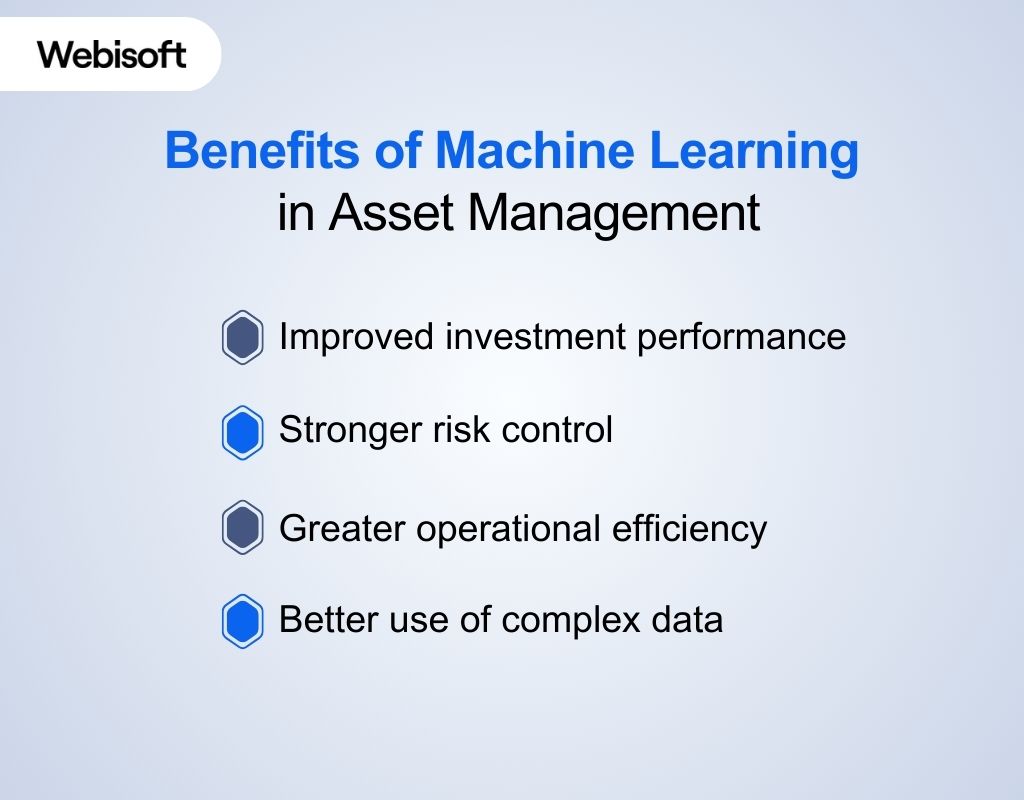

Benefits of Machine Learning in Asset Management

Machine learning in asset management improves how firms make decisions, manage risk, and operate efficiently in complex markets. More investment teams are adopting AI and ML because of measurable advantages in performance and productivity.

A global survey found that 9 in 10 asset managers are either already using AI or planning to adopt it in their investment strategy or research. So what are the real benefits? Let’s find out:

Improved investment performance

Machine learning helps teams uncover hidden patterns in large financial datasets that manual methods often miss. These insights support better return forecasts and help prioritize investments that align with risk tolerance.

Research shows that 67% of organizations are increasing investments in AI after seeing strong early value from such tools in investment workflows. Machine learning also reduces emotional bias in decisions.

Using data-driven signals instead of gut feeling improves consistency in portfolio construction and reduces costly judgment errors.

Stronger risk control

Machine learning strengthens risk monitoring by identifying unusual behavior in volatility, liquidity, and correlations. These models help risk teams detect stress patterns earlier than traditional indicators.

According to a global survey, over 90% of managers are already using or planning to use AI for research and strategy, including risk modeling. ML also supports scenario analysis. By simulating market stress patterns, teams better prepare portfolios for sudden shifts rather than reacting late.

Greater operational efficiency

Machine learning increases operational efficiency by automating repetitive tasks like data cleaning, risk checks, and report updates. Teams can then focus more time on strategy refinement than manual processing.

McKinsey & Company reports that AI applications have the potential to unlock productivity gains of 25% to 40% when applied effectively in investment workflows. This efficiency translates into faster research cycles and quicker portfolio adjustments.

Better use of complex data

Machine learning lets firms analyze both structured and unstructured data, such as prices, earnings call transcripts, and news sentiment. Firms that combine numeric and alternative data often gain richer market context. Surveys show this trend, as asset managers increasingly deploy ML to handle larger data volumes and improve insights. ML helps teams process data faster and more accurately, giving them clearer signals to base investment actions on.

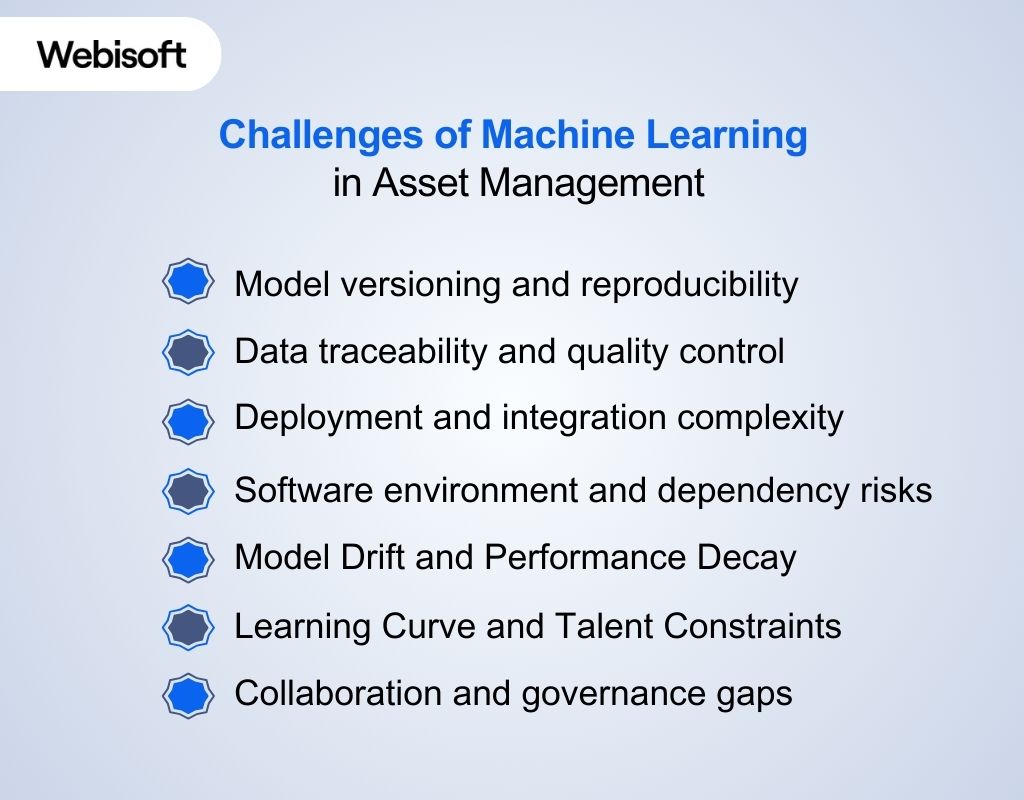

Challenges of Machine Learning in Asset Management

Machine learning in asset management faces operational and governance hurdles that often outweigh pure modeling issues. Many firms struggle not with algorithms, but with managing models, data, and infrastructure at scale.

Model versioning and reproducibility

Model versioning becomes a problem when teams cannot trace which dataset, parameters, or environment produced a portfolio signal. The Study found environment dependency and training configuration among the most discussed issues in ML systems. Reproducibility matters in finance because regulators and internal audit teams require traceable model decisions. If a firm cannot recreate results, compliance risk increases.

Data traceability and quality control

Data traceability breaks down when datasets evolve without tracking changes. The study highlights data management and dataset handling as major pain points for ML practitioners.

In asset management, even small data errors distort return forecasts and risk models. Data leakage during training can inflate backtest results and mislead portfolio decisions.

Deployment and integration complexity

Model deployment often fails at the handoff between research and production systems. Study shows deployment and service configuration as top recurring discussion themes.

When infrastructure lacks stability, trade execution and portfolio updates suffer. This increases operational risk in live markets.

Software environment and dependency risks

Software dependency conflicts frequently disrupt ML workflows. Small library mismatches can break model pipelines. In asset management, even short downtime affects reporting cycles and client confidence.

Model Drift and Performance Decay

Model drift becomes a silent threat when market conditions change. A model trained on stable volatility regimes may fail during sudden macro shifts. Financial markets evolve due to policy changes, liquidity cycles, and global events.

If firms do not monitor prediction accuracy continuously, performance slowly degrades without immediate detection. This drift increases exposure to unseen risk. Ongoing validation and retraining protect portfolio stability.

Learning Curve and Talent Constraints

The learning curve slows adoption inside traditional investment firms. Portfolio managers often understand markets deeply but may lack technical ML expertise. Building reliable ML systems requires data engineers, ML engineers, and risk specialists working together.

Without structured onboarding and cross-team training, projects stall or fail to scale. Firms must invest in internal capability development alongside technology adoption.

Collaboration and governance gaps

Collaboration issues slow ML adoption inside investment firms. Teams often lack shared experiment tracking, documentation, and lifecycle management systems. Governance also raises pressure. Regulators increasingly demand transparency in AI-driven financial systems.

Without explainability and proper oversight, firms face regulatory scrutiny. Machine learning in asset management offers strong potential, but operational discipline determines long-term success. Firms that solve versioning, traceability, and governance challenges gain sustainable advantages.

For teams seeking structured implementation support, contact Webisoft to design controlled data pipelines, managed model lifecycles, and compliance-ready ML architecture aligned with investment operations.

That practical, engineering-led approach helps investment teams adopt machine learning responsibly without increasing operational risk.

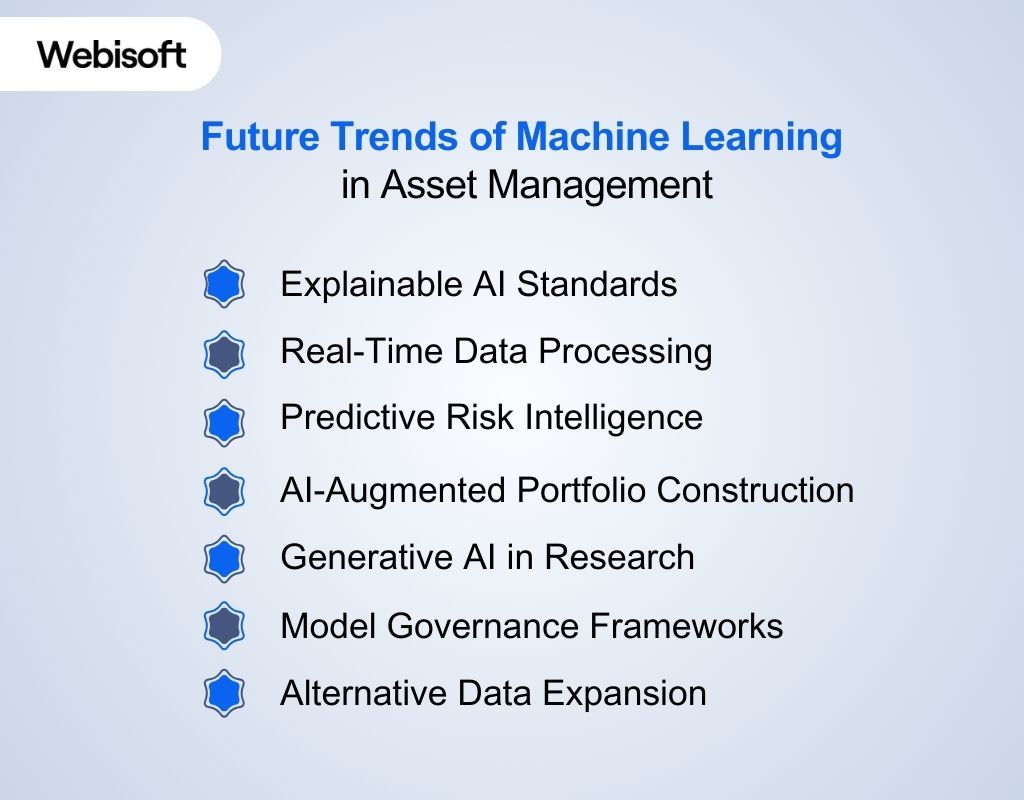

Future Trends of Machine Learning in Asset Management

Machine learning in asset management is entering a more disciplined stage. Early adoption focused on improving forecasts, but firms now care just as much about control, transparency, and risk management. As models move into live trading and portfolio systems, expectations change.

The future will revolve around explainability, real-time intelligence, structured governance, and scalable data integration across investment operations:

Explainable AI Standards

Explainable AI will become mandatory in regulated investment environments. The U.S. SEC has proposed new rules on predictive data analytics to address conflicts and transparency in AI-driven advice (Source: SEC, 2023).

Explainability allows firms to justify why a model signaled a trade or adjusted portfolio weights. This reduces compliance risk and strengthens audit trails. Regulators increasingly expect traceable model reasoning rather than opaque outputs.

Real-Time Data Processing

Real-time processing will define competitive positioning. Markets now generate continuous price feeds, macro releases, and sentiment signals that shift intraday risk exposure.

Firms that process data instantly can adjust portfolios before volatility compounds. Live data pipelines allow dynamic monitoring of liquidity, correlation breakdowns, and drawdown risk.

Predictive Risk Intelligence

Predictive risk intelligence will replace static backward-looking models. Traditional risk metrics often rely on historical variance, which fails during regime shifts.

Modern ML models combine volatility clustering, macro signals, and cross-asset behavior to identify instability early. This allows proactive exposure reduction instead of reactive loss management.

AI-Augmented Portfolio Construction

AI will increasingly support portfolio allocation decisions. Instead of periodic rebalancing, dynamic allocation models will respond to structural market changes.

These systems rank assets, simulate forward scenarios, and optimize risk-adjusted exposure faster than manual workflows. Portfolio managers still make final decisions, but they rely on structured quantitative insights.

Generative AI in Research

Generative AI will streamline investment research. Large language models can summarize earnings calls, extract key themes from filings, and compare management tone across sectors. This shift increases analyst productivity while preserving strategic oversight.

Model Governance Frameworks

Model governance will become central to machine learning maturity. Firms must track model versions, training datasets, deployment environments, and performance drift.

A 2024 study found environment dependency, deployment complexity, and version management among the most discussed ML operational challenges. Strong governance prevents reproducibility failures and reduces operational breakdowns in production systems.

Alternative Data Expansion

Alternative data will continue expanding beyond price and balance-sheet metrics. Satellite imagery, transaction data, digital engagement trends, and supply chain signals increasingly feed predictive systems. Machine learning in asset management enables firms to integrate structured financial metrics with unstructured real-world signals at scale. The advantage lies in processing complexity faster and more consistently than manual analysis.

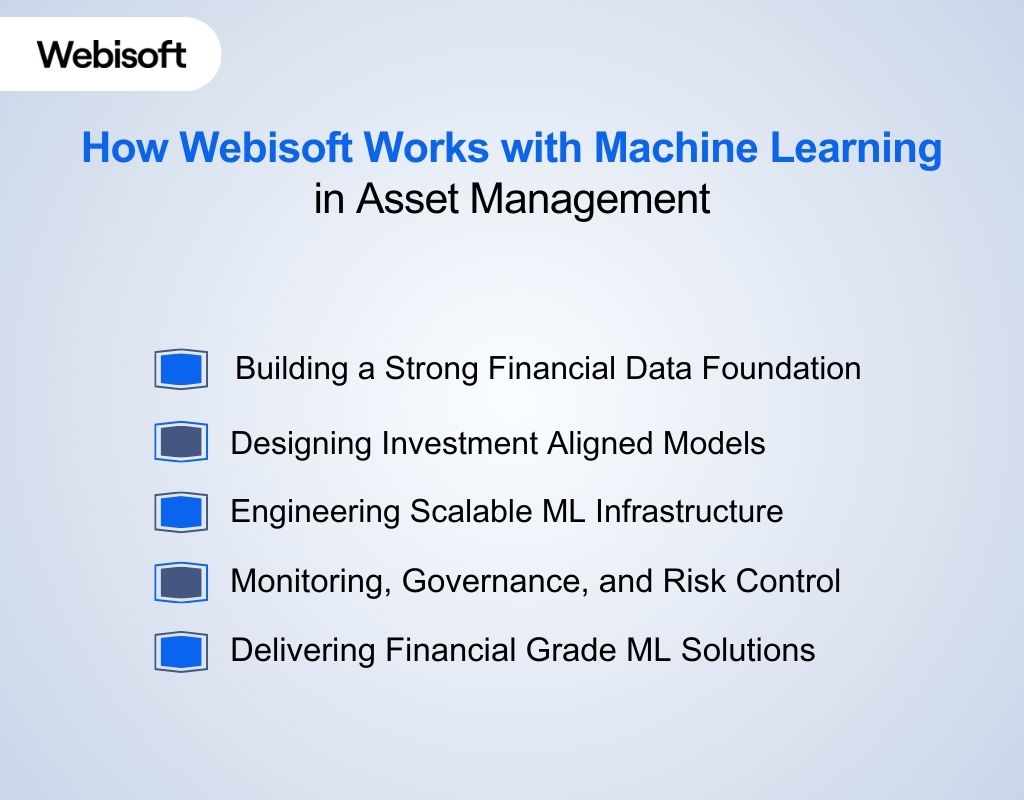

How Webisoft Works with Machine Learning in Asset Management

Machine learning in asset management requires more than building models. It requires data discipline, financial domain knowledge, and production-level engineering. Webisoft approaches this work as a full lifecycle system, from data design to live deployment.

Building a Strong Financial Data Foundation

Successful ML systems start with structured and validated financial data. Webisoft engineers design pipelines that collect market prices, macro indicators, and fundamental metrics in a consistent format. Clean data reduces model instability and prevents misleading backtests.

Financial regulators and global institutions continue to stress data governance in AI systems. That is why every dataset goes through validation checks before model training begins.

Designing Investment Aligned Models

Machine learning models must reflect real portfolio objectives. Webisoft structures supervised, clustering, or time series models around clear targets such as return ranking, volatility prediction, or drawdown control.

This ensures outputs connect directly to portfolio decisions instead of abstract research metrics. Each model includes validation layers that test robustness across different market conditions. This reduces overfitting and improves reliability during live deployment.

Engineering Scalable ML Infrastructure

Production readiness defines long-term success. Webisoft implements cloud based systems with version control, experiment tracking, and automated retraining workflows. These controls address common deployment failures reported in recent 2024 research on ML asset management systems.

Stable infrastructure allows models to update safely when market data shifts. This prevents downtime and signal drift.

Monitoring, Governance, and Risk Control

Live ML systems require ongoing oversight. Webisoft integrates monitoring tools that track model drift, exposure changes, and performance decay in real time.

This helps investment teams respond quickly when signals weaken. Transparency also remains essential. Documentation, audit logs, and validation reports support internal review and regulatory requirements.

Delivering Financial Grade ML Solutions

Machine learning systems must integrate with trading platforms and reporting dashboards. Webisoft connects predictive models directly to execution systems and portfolio analytics tools. This creates a seamless workflow from research to decision-making.

The goal remains simple. Machine learning should improve clarity, speed, and risk awareness in asset management without adding operational instability.

Conclusion

Machine learning is no longer a research experiment in investment firms. It has become a practical tool for improving portfolio construction, risk monitoring, and execution discipline when applied correctly. However, success depends on clean data, strong governance, and realistic expectations about model limits.

Firms that treat ML as a full lifecycle system, not just a prediction engine, gain stronger long term value. They focus on validation, monitoring, and integration with real investment workflows instead of chasing short term backtest gains.

Machine learning in asset management delivers results only when it aligns with portfolio objectives, regulatory standards, and operational stability. When implemented with discipline, it strengthens decision making without increasing fragility.

FAQs

Machine learning does not replace portfolio managers. It supports them by analyzing large datasets faster than humans can. Human judgment remains critical for strategy decisions, regulatory responsibility, and client communication.

Machine learning models can improve forecast accuracy, but they are never perfect. Performance depends on data quality, validation methods, and changing market regimes. Models can fail during extreme events if firms do not stress test them properly.

Small firms can use machine learning through cloud platforms and open source tools. Cloud infrastructure reduces hardware costs and allows firms to scale gradually. However, firms still need clean data and skilled professionals to manage the lifecycle.

Model risk increases when firms rely too heavily on historical data. Overfitting, data leakage, and poor explainability can lead to unstable results. Strong governance and monitoring reduce these risks.

Implementation time depends on data readiness and internal expertise. Firms with structured data pipelines move faster than firms with fragmented systems. A clear roadmap shortens deployment time and improves adoption.